Declare Your Financial Independence

With today being the 4th of July and the 250th anniversary of the founding of our country, we wanted to focus today’s post on Independence. Specifically, Financial Independence.

Take a minute to put yourself in the shoes of the Patriots of America. They felt oppressed. They wanted freedom. They wanted liberty. They wanted control of their own county. They wanted to live life how they wanted to, on their own terms. They met behind the scenes and developed a plan; they developed clarity on what would be needed to achieve freedom. Most importantly, they acted. They defied, they fought, they held strong until the ultimate battle was won. It took time, perseverance, focus, and discipline to achieve independence. They won freedom and opportunity that we enjoy to this day.

An important note on the 4th of July is that our Founding Fathers agreed on the principles of the Declaration of Independence, but that didn’t end anything. They fought Britain for another 7 years until ultimately reaching independence. The declaration is very important. The declaration gave clarity and focus for what they were after. A declaration causes a mental shift. They weren’t just interested in independence, they were committed. They were willing to fight and die for independence.

Our mission at MFF is to help you reach Financial Independence. But we cannot fight the fight for you. When you go through our core course, The Standards of Financial Literacy, you are given the tools to reach financial independence. But there’s got to be something in you that decides you truly want it. If you stick with the principles you’ve learned, you can achieve it, but will you stick it out? Are you willing to fight for your independence? You need to decide if you’re just interested in financial independence or if you’re committed to getting there.

Today, I’m asking you to Declare Your Financial Independence!

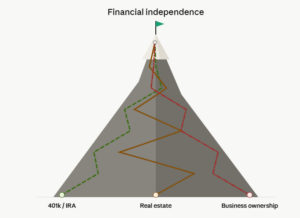

So, what is financial independence? We define financial independence as accumulating enough assets that passively generate income to support your lifestyle without you having to work and earn income any longer. Your assets could be money invested in a 401k/IRA that you have accumulated enough that you can safely withdraw each year and not deplete the account, real estate investments that yield rental income, or businesses that passively pay you, with you not actively running the operation any longer.

Each path has its own difficulty that you’ll need to overcome to reach the top. You’ll need to stay disciplined. You will need to take some risk. You’ll need to consistently set aside money for the future. One day, your assets will accumulate enough that they’ll support you, and you’ll officially reach the top of the mountain, Financial Independence:

Your path will vary based on your personality and risk tolerance. Some people value stability. They may want a stable W-2 income salary job where a company provides a great 401k match program that you can consistently contribute to. Some are more entrepreneurial and value freedom. They want to found their own business or invest in real estate that they plan to grow into a profitable venture that yields strong cash flow and possibly sell in the future. Each path has its own challenges and risks.

That’s why we teach you to take multiple paths. The principle of diversification shields you from risk in both investing and earning income. What if the bridge collapses on the path you’re taking to the top? You’re going to need to shift to a different path. Sometimes things won’t go to plan in your working life: the economy could have a recession, your company could have layoffs, technology could make your skillset obsolete, etc. Having multiple income streams helps you ensure income is still coming in case one of your streams dries up. A good start for a second stream of income is to have some money in a savings account and the bank is paying you interest. Perhaps you can add a side hustle to your main job, collect rental income, or get a roommate.

For most people, you’ll have your primary source of earned income that will generate the majority of your income to start. You either went to or are going to college or a secondary training school to learn a skill set that will get you a degree or credential that gets you a good job that earns you an income that you’re happy with to start. A good job means different things to different people. You can value different things such as income, commute, hours, benefits, promotion opportunities, etc. When you’re starting your career, you will likely need to make some sacrifices. You may need to work extra hours, coming in early, staying late. You should plan to show initiative and do work beyond what’s asked of you to earn respect at your workplace and get on the path towards rising up at your company.

Your 20’s are a very important time in your career. Yes, it’s a fun time in your life. You have just graduated from college, you are earning more than you ever have, and there are a lot of things to do and the world to see. But it’s also a rare and fleeting time to buckle down, get great experience, and seek to earn as much as you can. You have less responsibility in your 20’s than you will in your 30’s, 40’s, and beyond. You might not be married yet or have kids of your own. You have the time and opportunity that you might not have later in your life. Take advantage of it.

You need a plan. A budget is your plan to start. People tend to focus a lot on the income different jobs can earn, but it’s not all about what you make – it’s what you keep at the end of the month. If your personal budget were a business, if you were “You, INC” – would your business turn a profit each month?

Envision Your First Full-Time Job

Imagine you have just graduated and landed your first professional role. Research what you might realistically earn in your field of interest (or a general entry-level business position if undecided).

- Use sites like MyNextMove, Glassdoor, Indeed, Salary.com, for starting salary data.

- Consider factors like your major, location (e.g., cost of living in the area you want to live), and entry-level roles such as business analyst, sales, marketing, finance, or operations.

- Aim for a realistic gross annual salary (before taxes). A good national ballpark for recent grads is around $40,000–$70,000 depending on the field, but adjust based on your research.

- Calculate Take-Home Pay Estimate your monthly net (take-home) income. Subtract approximate taxes, health insurance, and retirement contributions (many employers withhold ~20-30% for these). The budget calculator will help with this.

- Use Our Budget Calculator Go to: https://morganfranklinfoundation.org/calculators/budget-calculator/

- Input your estimated monthly income (wages/salary + any other sources).

- Estimate your monthly expenses in each category (housing/rent, utilities, transportation, food/groceries, dining out, insurance, debt payments like student loans, savings, etc.). Be honest and realistic—research typical costs in your expected living area.

- Common categories for recent grads often include: rent (~$700–$1,500+), transportation, groceries (~$300–$500), utilities, phone, insurance, and student loans.

- Review the “Money Leftover” result and the suggested next steps on the page.

- Other factors to consider: Will you live at home? Will you have a roommate? Make sure to compute annual costs to a monthly payment such as Student loans, car payment, credit cards, etc

What is your number?

As mentioned before, there are 3 paths to the top of the mountain that get you to financial independence. And they all look different when you’re at the top too. You need to determine the path you’re taking and what it will look like for you at the top.

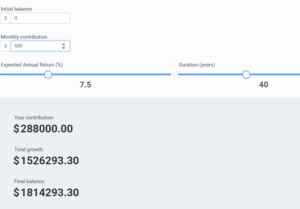

If you’re taking the 401k/IRA path, you need to know how much money you need to invest in those accounts to yield the amount of money you need per year to live through retirement. To get this number, you need to understand your monthly/annual budget from the Budget Calculator. If, for example, you determine you need $6,000 a month you can use that to build how much you need to save for retirement. A simple way to calculate your number is to take ($6,000 x 12) = $72,000. Now take $72,000 x 25 = $1,800,000. In retirement, your investment account should be able to yield you 4% a year in interest and dividend payments, which will safely allow you to withdraw 4% per year without digging too far into your principal account. $1,800,000 x .04 = $72,000 or $6,000/month. Keep in mind this is slightly simplified, as inflation will keep increasing and it doesn’t factor in Social Security income.

Now that you have your number, you can input how much you’re able to invest per month into our Investing Calculator. Typical returns you can forecast are 6% – 8%. This will tell you how much you need to aside each month and for how long to get to $1.8M. From my calculations, starting with $0 today, it would take $600/month, earning 7.5%/year, for 40 years to earn $1.8M. So you want to start as early as possible!

But what about the other paths?

So now you know you’re looking for $6,000/month. You can also think through what type of business could yield $6,000/month. If one rental property earned you a cash flow of $2,000/month, could you find two other similar properties to get to $6,000/month? How much money would you need to save as a down payment for the first rental property? Could you also live in it and try house hacking?

Maybe you’re really good with video work and started a business where people pay you to do video work for them. You could also upload your own content to YouTube and now YouTube pays you a monthly amount for people watching your videos. There are also monetary opportunities with video on Facebook, X, Instagram, and TikTok. This is how artists and creators get paid. Every time you watch a video on Youtube or listen to a song on Spotify, that artist or creator has the opportunity to earn income. There are a lot of problems to solve for other people; problems are business opportunities. the bigger the problem you solve, the more money people will pay you to do it.

So there you have it, you have the tools, you have the ideas, but knowledge is nothing without action. Will you take the time to set your goals, determine what your number is, and work towards that goal? Will you Declare Your Financial Independence? No one is going to take care of you like you. Will you fight for your financial independence? It’s entirely within your reach. Others have done it. We believe you can do it too.